LikeFolio's MegaTrends June update for hedge funds highlighted some unbelievable […]

Beyond Meat (BYND) is Facing Serious Headwinds…

April 22, 2022

When it comes to investing, it’s important to not take things personally.

Even when you really like (or don’t like) a company.

But that doesn’t mean I couldn’t profit from Beyond Meat’s blistering rise.

AND its slow-burn back down.

In fact, thanks to LikeFolio's real-time consumer insights, members were able to do just that.

Because LikeFolio wasn’t just listening for MY opinion on Beyond Meat. It was listening to the collective voices of millions of consumers, and recording how loud the voices were over time.

The initial frenzy is how LikeFolio was able to issue a Bullish Alert for Beyond Meat, very shortly after the company’s IPO (June of 2019) when shares were trading near $96.

In the months to follow, BYND shares would gain as much as +144% in value!

And it’s also how LikeFolio knew…the initial curiosity spark was dying down.

We issued a BYND BEARISH alert in October 2020. Right now, shares are trading around -77% lower.

So…is the (fake) bleeding done for this company?

LikeFolio data suggests…maybe not.

Here are three reasons why I’m still staying away from BYND.

1. Consumer Demand Growth is Waning after a Temporary Product Pop

Beyond Meat began launching meat-free “chicken tenders” in grocery stores in October of last year.

While the product launch generated some chatter among consumers, the mention volume has since normalized lower, currently averaging less than a mention a day.

Beyond also launched a “chicken” product in KFC restaurants nationwide to kick-off 2022.

While both products generated a small bump in consumer demand, these levels are dropping.

Even considering these new product launches, BYND Purchase Intent Mentions have dropped by -21% on a YoY basis.

What’s going on?

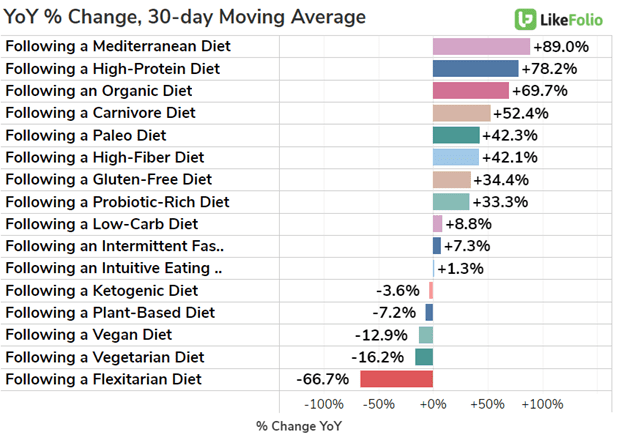

2. Plant-Focused Diets are Losing Momentum

This doesn’t mean that vegans and vegetarians have jumped ship…but it does suggest that consumers are joining the plant-based team at a slower clip…not a great sign for explosive growth.

You can see a dramatic shift in YoY mentions on the chat below for:

- Following a Plant-Based Diet

- Following a Vegan Diet

- Following a Vegetarian Diet

- Following a Flexitarian Diet

Meanwhile, MORE consumers are following a high protein, and even organic diet.

These are some challenging headwinds for a plant-based company expected to return to growth in 2022.

And while Beyond may receive a short-term boost from its new food-service product line, its retail sales forecast looks a bit more grim.

Last quarter, U.S. retail sales fell -20% …and it’s the company’s most important segment.

Unfortunately, LikeFolio data paints an uphill battle in the grocery store aisles.

Not only is Beyond Meat losing steam to other plant-based competitors (namely, Impossible Foods), but food item pricing is rising across the board.

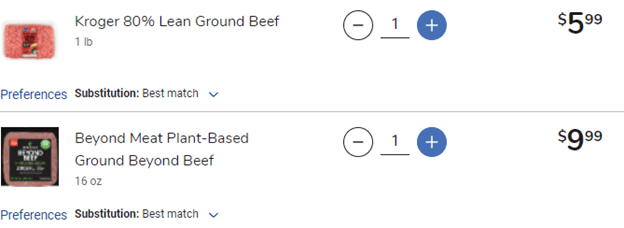

3. Rising Grocery Costs Weigh on Consumers

Inflation is trickling into the grocery aisle, with consumer mentions of rising food costs up more than +150% YoY. Beyond Meat was already struggling to achieve price parity with traditional ground beef.

Let me paint the picture.

Right now at my local Kroger, I can buy one pound of ground beef for almost half the price of one pound of Beyond Beef.

That’s a tough call to make if you are a consumer on a budget. These folks agree:

Want deeper insights? Get Free Access to The Vault.

Tags: