Black Friday Weekend (leading into Cyber Monday) can make or […]

Target (TGT) has a Logistical & Reopening Advantage

May 18, 2021

Target (TGT) has a Logistical & Reopening Advantage

But will it be enough?

Last quarter, Target was boosted by a strong holiday season and surge of stimulus-induced shopping: comp sales increased +20% YoY An increase in average ticket size (+13%) and foot traffic (+6%) contributed to this growth, but the standout driver was digital sales.

- Digital sales accounted for 2/3 of Target overall comp growth, increasing +118% YoY

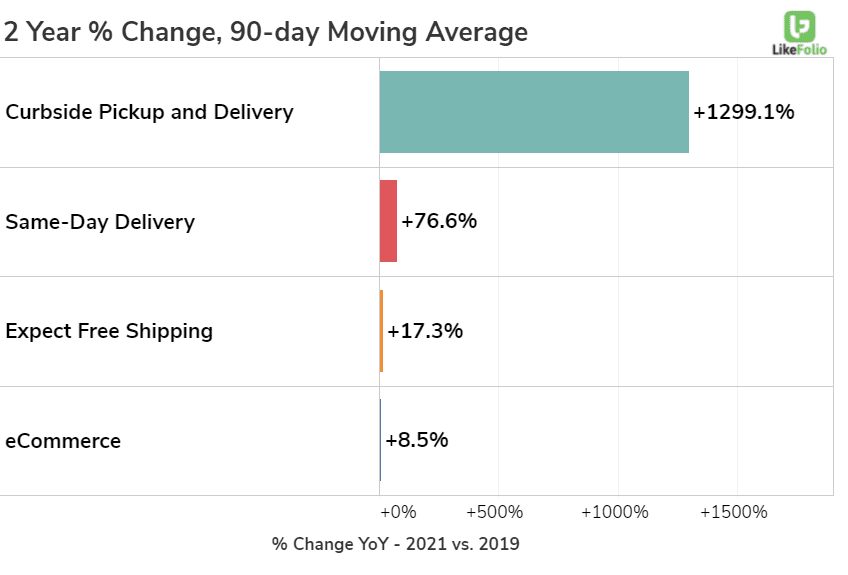

- Same-Day Services (order pick up, drive up, Shipt) increased +212% YoY.

Target is able to ramp these segments so efficiently because 95% of sales were fulfilled by Target stores....a huge logistics advantage vs. a company like Amazon. Same-Day Delivery and Curbside Pickup mentions hold the most significant demand growth in the LikeFolio universe when it comes to order fulfillment vs. pre-Pandemic levels.

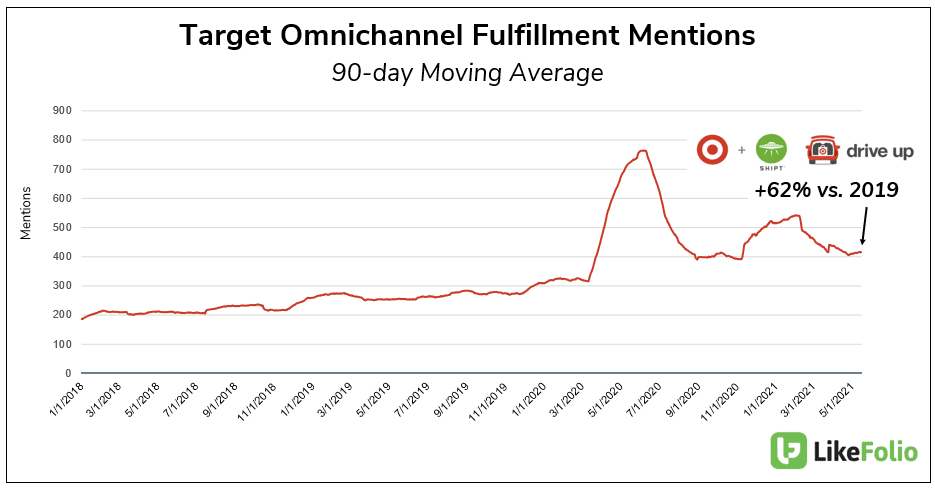

LikeFolio data shows continued omnichannel expansion for Target. Onboarding mentions surged during Covid making YoY growth comps tough, but these mentions remain +62% higher vs. 2019 levels. Translation: stickiness.

Target is also doing a great job with owned brands: Good & Gather Mentions (grocery items) have increased +56% YoY, now generating more than $1 billion in annual revenue. Walmart just posted a significant earnings beat, and shares traded up slightly (+3%). The company also raised guidance, citing pent-up demand as localities reopen. This will be a significant goal post to follow, but Target does have an advantage in reopening segments: Apparel and Beauty. Target Apparel Mentions have increased +21% QoQ as social events open up, and Beauty mentions have increased +4% QoQ. Target's Earnings Signal is Neutral ahead of earnings (-18) with a slight bearish lean. While we think Target is going to post a great report, it may not prompt a breakout above all-time highs. Any pullback could be an opportunity for long-term investors.